Tariffs, Reindustrialisation, and the Dollar: Geopolitical Implications of US Economic Strategy under Trump

/By Andrea Montiglio, edited by Alina Hueber

1. Introduction

The return of Donald Trump to the White House marked a significant shift in American economic and geopolitical strategy. Through the introduction of tariffs, industrial policies, and calls for a weaker dollar, the Trump administration has increasingly framed trade deficits, deindustrialisation, and external dependencies as threats to US national security and long-term strategic power.

However, these policies may conflict with some of the structural foundations of the international economic and financial order that has sustained American global primacy since the end of the Cold War. This article argues that efforts aimed at reducing US external deficits and restoring domestic industrial capacity could generate broader geopolitical consequences, potentially weakening the international centrality of the US dollar, encouraging dedollarisation dynamics, and accelerating demands for greater strategic autonomy among US allies and competitors alike.

2. The Strategic Shift in US Economic Policy

In April 2025, Donald Trump announced general global tariffs at 10% for any imported good into the United States of America, together with additional country-based tariffs for a number of countries. These tariffs target all US trading partners, without apparent strategic distinction between allied countries and competitors, with the European Union faced with a tariff rate of 20% (EO 14257, 2025). These tariffs were justified, in Trump’s view, by the fact that the US had been sustaining persistent goods trade deficits vis-à-vis its trading partners, which maintained much higher tariff rates and imposed greater technical barriers to trade than those of the US. These asymmetries would have resulted in structural damage to US exports and the country’s production capacity, a loss of manufacturing jobs, and a dependency on imports in critical supply chains, including the American defence-industrial base. They therefore constituted an “unusual and extraordinary threat to the national security and economy of the United States” (EO 14257, 2025). These vulnerabilities, according to Trump, were particularly exposed during recent global crises, such as the COVID 19 pandemic and the disruptions to global trade caused by Houthi attacks on merchant vessels in the Middle East (EO 14257, 2025).

In addition to the abovementioned general tariffs, in June 2025 the Trump administration introduced a new round of tariffs targeting specifically aluminium and steel imports, raising tariff rates for related products from 25% to 50%, and marking an escalation in American trade policy. These tariffs too were justified by the defence of US national security, invoking section 232 of the Trade Expansion Act of 1962 (Proc. 10947, 2025). They aimed at ensuring sufficient domestic production levels of steel and aluminium, which is crucial not only to meet the needs of the American defence industry, but also to maintain a manufacturing capacity in other strategic sectors, such as shipbuilding.

This approach marked a paradigm shift in the new US administration’s view of the international order, which appears to be increasingly willing to turn to protectionist measures and reduce interdependence between nations. Since the end of the Cold War, the United States promoted and implemented an international economic and financial system based on open and free trade and the centrality of the US dollar. One of the core implications of this system was the presence of a constant US trade deficit, which was only partially compensated by a surplus in the balance of services. The persistent US trade and current account deficits were mirrored by sustained capital inflows into US financial markets, in particular Treasury securities and other dollar-denominated assets (Obstfeld and Rogoff, 2005, p. 133). This dynamic was allowed by the strength of the dollar in the international system and its role as reserve currency, underpinned by US military and diplomatic power and the institutional stability of the country (Eichengreen, 2011). In this context, US governments were able to finance external deficits through foreign purchases of US financial assets, borrowing capital from international financial markets at relatively low interest rates, sustaining a growth model heavily reliant on domestic consumption and reinforcing the international diffusion of the dollar.

While this system reinforced American hegemony, financial dominance, and soft power, it also generated important structural imbalances within the US economy. The globalisation model promoted by the United States after the Cold War strongly benefited the financial sector and American consumers through cheaper imports and sustained capital inflows (Eichengreen, 2011). However, it also contributed to the long-term erosion of domestic industrial capacity in several strategic sectors, increasing US dependence on foreign supply chains for critical goods and raw materials (Farrell and Newman, 2019). In the view of Trumps administration, these vulnerabilities have strategically weakened the United States, in particular vis-à-vis its main strategic competitor, China. US dependence on Chinese imports in sectors such as rare earths and critical supplies increased significantly, while China significantly outpaced the US in the share of global industrial output, particularly in strategic sectors like shipbuilding. Based on recent analysis, today China accounts for over 50% of total global shipbuilding capacity, while the US just accounts for 0.1% (CSIS, 2025).

3. The Structural Foundations of Dollar Hegemony

3.1. The Dollar-Centred International Order

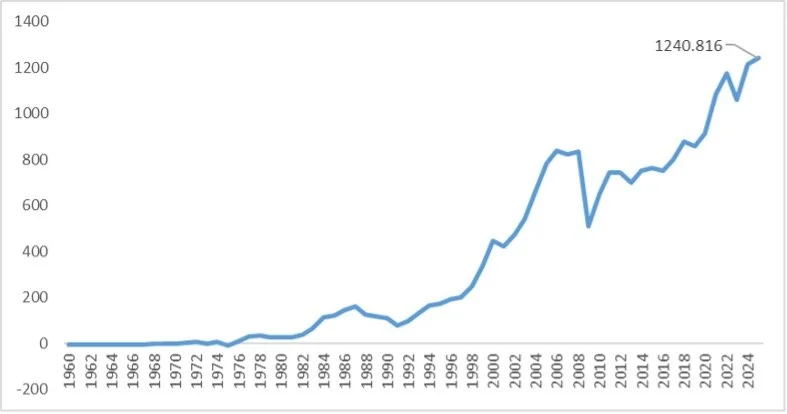

Since the end of the Cold War, the US has run a persistent goods trade deficit. As data from the US Bureau of Economic Analysis show, the US trade deficit widened significantly from the mid-1990s onward: from a deficit of around 76 billion in 1991, it reached a record figure of $1.24 trillion in 2025.

Figure 1: US goods trade deficit, 1960–2025 (billions of US dollars) (US Bureau of Economic Analysis, 2025).

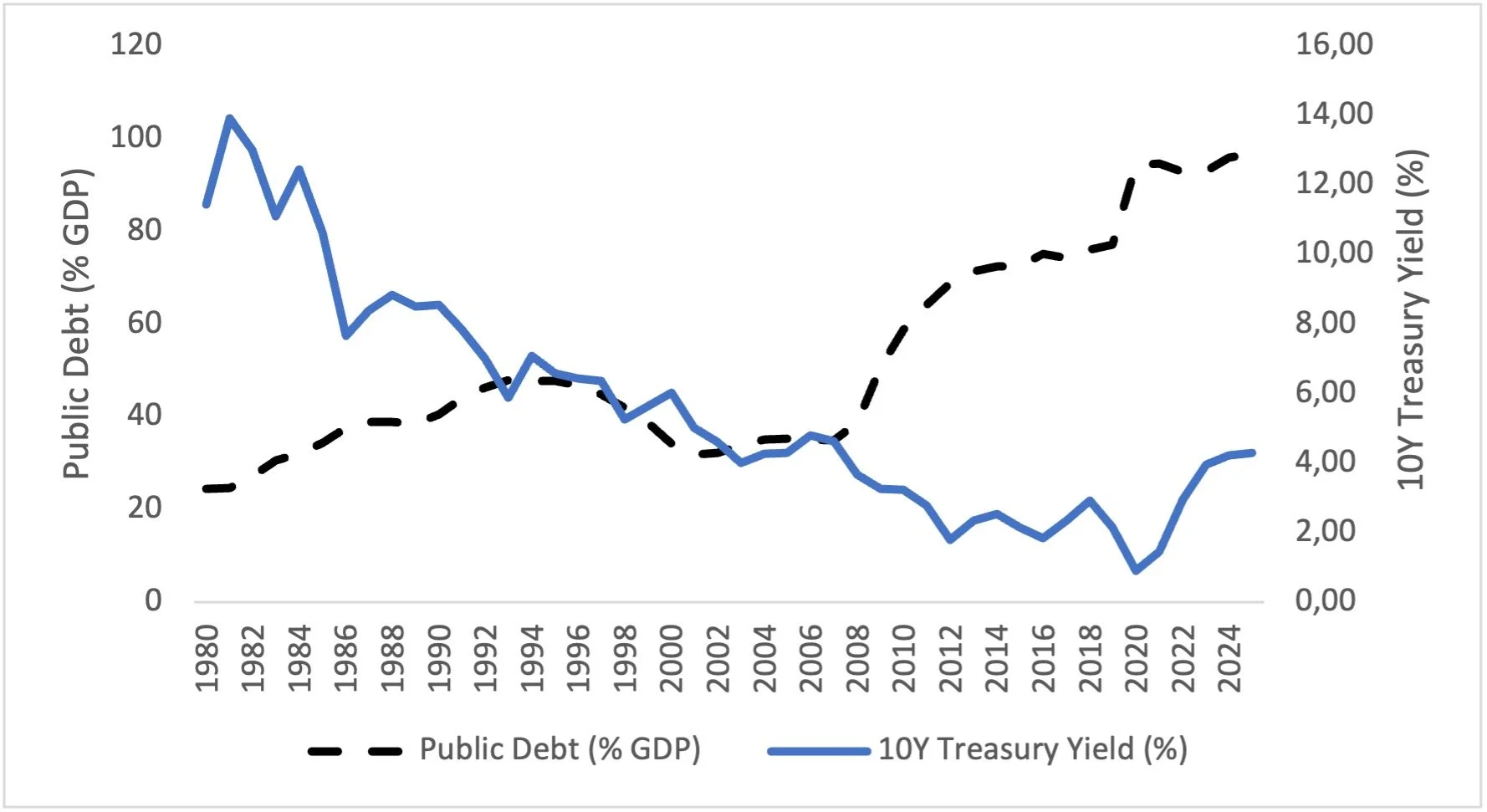

To offset these deficits and maintain balance in the balance of payments, the United States consistently recorded a surplus in financial account, supported by capital inflows into US financial markets, particularly into US Treasury securities. This, in turn, contributed to an increase in US public debt levels. However, despite record levels of public debt and the increasing supply of Treasuries, yields on US government bonds remained at relatively low levels – with the important exception of the post-Covid period – thanks to a persistently high global demand for US dollar-denominated assets. The following figure shows that increases in US public debt (as a percentage of GDP) were associated with a paradoxical decline in interest rates on US Treasury securities.[1]

Figure 2: US public debt (% of GDP) and 10-year Treasury yield, 1980–2025 (FRED, 2025a; FRED 2025b).

In most advanced economies, rising public debt and persistent current account deficits would have typically led to higher borrowing costs in financial markets, as well as pressure on the exchange rate. The United States, however, was able to sustain these imbalances without facing a debt crisis or significant currency depreciation. The anomalous relative strength of the US dollar can be seen when the currency is analysed through the lens of the purchasing power parity (PPP) theory. Following the PPP theory, over the long run a currency should present the same purchasing power both in the domestic country and in a foreign country, and the exchange rate should therefore reflect the relative purchasing power of the two countries’ currencies (Krugman, Obstfeld and Melitz, 2018, Chapter 16). However, a comparison between the EUR/USD exchange rate predicted by purchasing power parity – using Germany as case study – and the actual market exchange rate based on 2024 levels shows that the dollar remains considerably stronger than would be expected based on relative prices between the two economies. In particular, the PPP deviation ratio is approximately 1.32 for Germany, while it settles at 1.18 in comparison with the United Kingdom.[2] This indicates that the value assigned to the dollar in international financial markets exceeds the level justified purely by purchasing power. Relative to currencies such as the euro and the pound sterling, the US dollar appears therefore to be moderately overvalued. In practical terms, this also implies that the nominal size of US expenditures – including in strategically relevant sectors such as defence – may overstate the country’s actual capacity to purchase real quantities of goods and resources at the international level.

This relative strength of the US dollar can be explained by its role as reserve currency and its centrality in the international commercial and financial system (Eichengreen, 2011). In fact, the US dollar remains the main currency held in foreign currency reserves by central banks worldwide, accounting for approximately 57% of total allocated reserves globally, against around 20% for the euro and 4.6% for the pound sterling, although a gradual downward trend has been observed in recent years (IMF, 2025). Moreover, the dollar is the currency used in most international trade transactions, and it also serves as the principal pricing currency for most commodities traded globally, including Brent and WTI crude oil, gold and silver, and several agricultural products. In addition, US Treasuries are widely regarded as safe assets by international investors, as they are highly liquid, easily tradable, and backed by relatively stable democratic institutions and a strong rule of law. As a result, global demand for US dollars remains consistently high, creating a self-reinforcing cycle in which the international strength of the dollar further increases global demand for dollar-denominated assets, thereby helping sustain the dollar’s global dominance.

[1] In particular, the graphic compares US federal debt held by the public as percentage of GDP (excluding intragovernmental debt) with the market yield on 10-year US Treasury securities.

[2] The PPP deviation ratio is calculated by dividing the actual market exchange rate by the exchange rate implied by purchasing power parity. A value above 1 indicates an overvaluation of the US dollar relative to the foreign currency considered (respectively EUR and GBP). Calculations based on data from World Bank and FRED databases. (World Bank, 2025; FRED, 2025c; FRED 2025d).

3.2. Exorbitant Privilege and Monetary Power

The implications of this system are profound. First, it allows the US to finance persistent fiscal and external deficits by issuing debt denominated in its own currency under highly favourable conditions. This dynamic is closely linked to the concept of “exorbitant privilege” originally coined by former French President Valery Giscard d’Estaing. The term refers to the willingness of foreign governments and investors to hold large quantities of US government debt at relatively low interest rates, due to the dollar’s status as the world’s primary reserve currency (Rogoff and Tashiro, 2015). This gives the US a degree of room for manoeuvre in monetary and fiscal policy that few other countries can enjoy. While other economies may experience balance of payments crises as a consequence of high levels of public debt and persistent external deficits, the United States is largely shielded from this risk due to the central role of the dollar in the international system, allowing it to finance its debt internationally through liabilities denominated in its own currency (Meyermans, 2014, p. 43).

Second, the United States retains considerable influence over global monetary conditions through the policy decisions of the Federal Reserve. This influence is exercised in several ways. When the Federal Reserve raises interest rates, capital tends to flow towards the United States, often leading to a strengthening of the dollar and to currency depreciation in other economies vis-à-vis the US dollar (Federal Reserve, 2022). Consequently, many countries are forced to adopt defensive measures, such as using their dollar reserves to stabilise exchange rates or tightening domestic monetary policy by raising interest rates themselves, thereby reducing their room for manoeuvre in economic policy (Obstfeld, 2015, pp. 8–11). In addition, as many countries hold substantial foreign exchange reserves in US dollars, including US Treasury securities, their exchange rate policies are partly constrained by balance-sheet exposure to US dollar assets and liabilities.

Also, many countries, particularly emerging economies, also hold significant portions of their public and private debt denominated in US dollars. As a result, tighter monetary policies in the United States and a stronger dollar can create financial pressures in these economies and may raise concerns over debt sustainability.

A further transmission channel of Federal Reserve policy into the international system is the pricing of commodities in US dollars. When the dollar appreciates, the price of dollar-denominated commodities increases in terms of foreign currencies, making imports of these goods more expensive for foreign countries. This may contribute to higher inflation and external imbalances in those countries. A prominent example of this mechanism can be observed in the Euro area during the 2021-2023 period, when a strong US dollar, combined with high global energy prices denominated in US dollars, contributed to significant import-driven inflation (ECB, 2023).

Finally, the centrality of the US dollar within the international financial system also provides the United States with significant geopolitical leverage. Because a large share of global financial transactions and cross-border payments are conducted in US dollars, the United States possesses an enhanced capacity to impose financial sanctions and restrict access to dollar-based financial networks (Zoffer, 2019, p. 152). This further illustrates how the strategic role of the dollar in the contemporary international order strengthens the ability of the United States to influence global economic and political outcomes.

3.3. The Triffin Dilemma and the Limits of Reindustrialisation

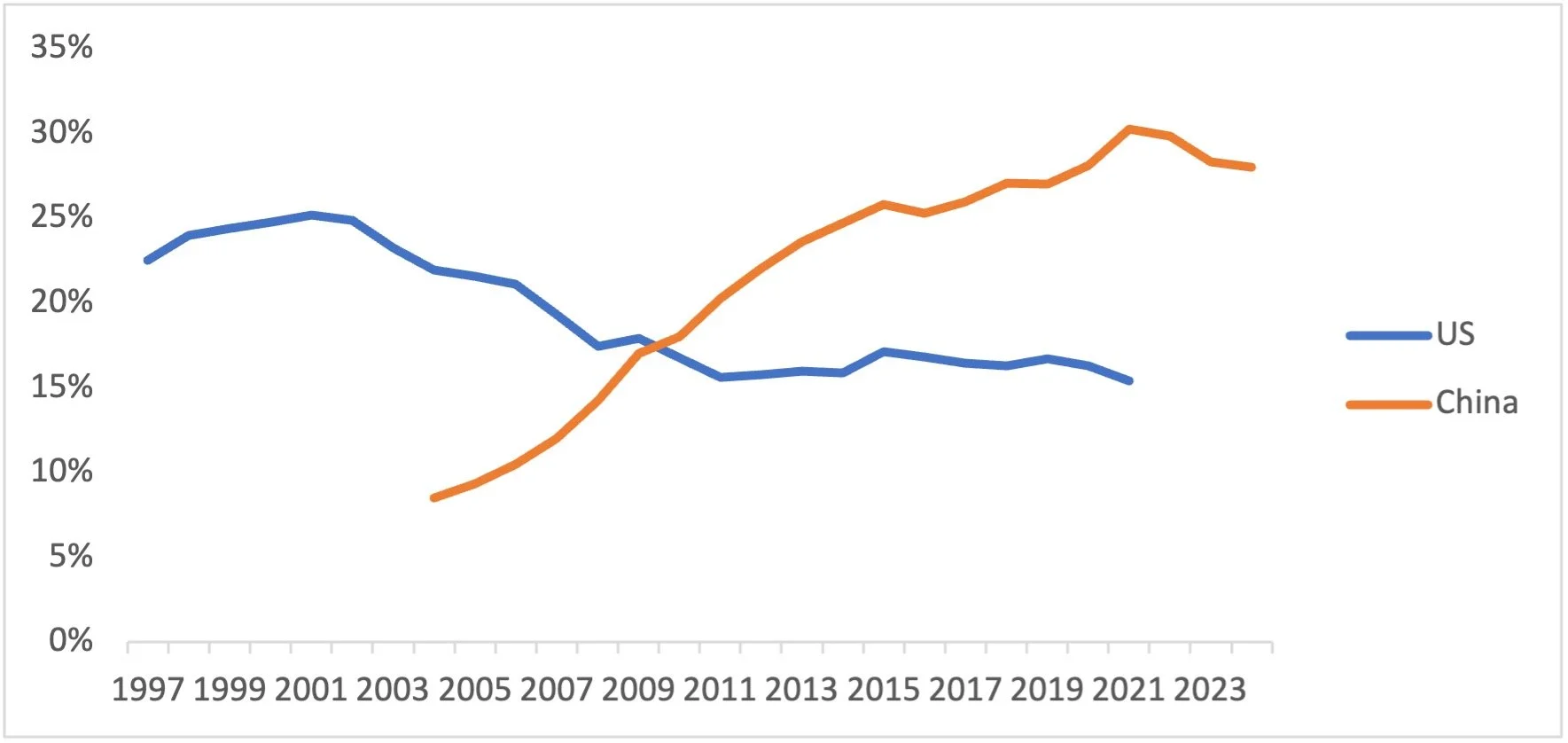

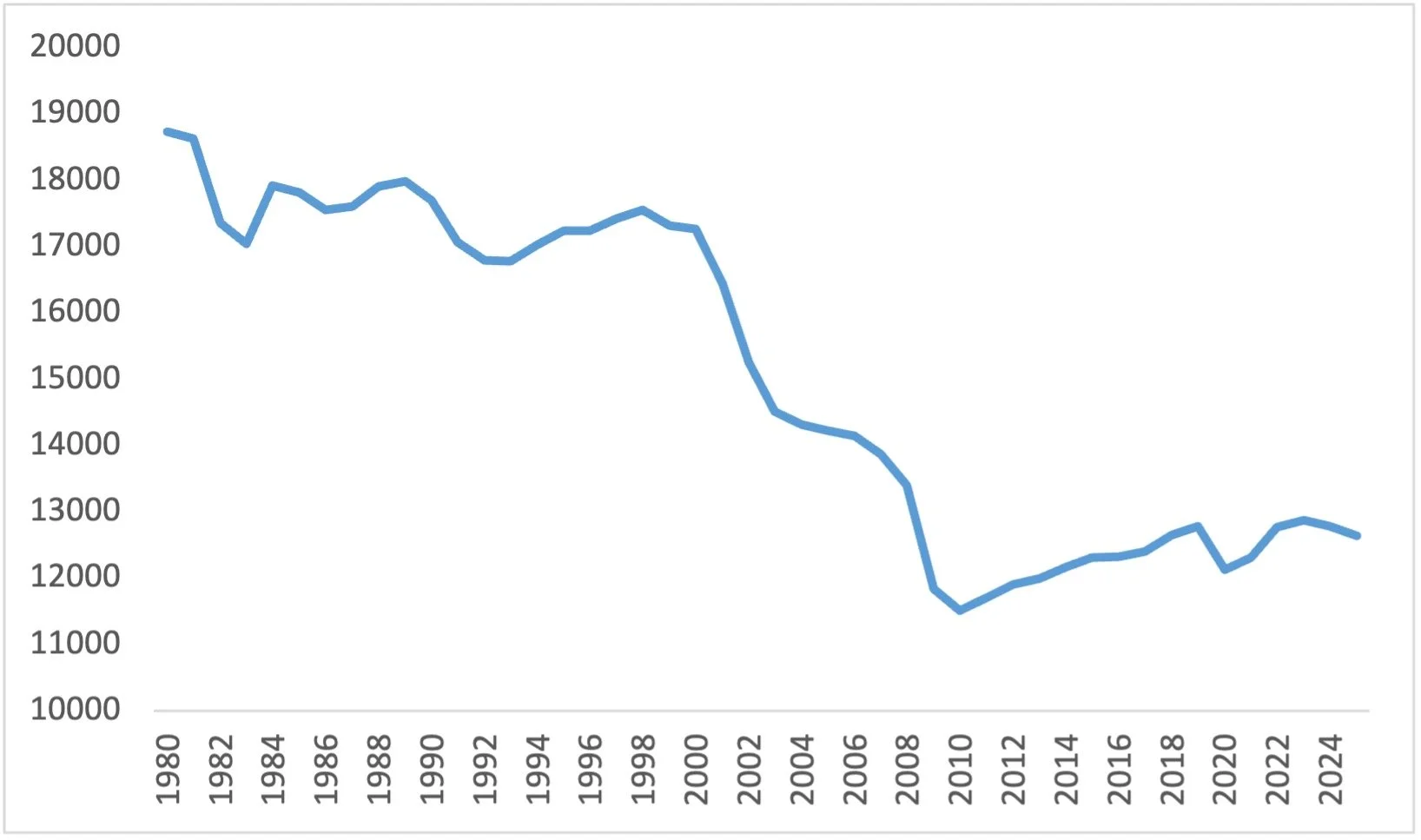

A persistent American external deficit has become a structural feature of the international economic and financial order over recent decades. Persistent current account deficits are mirrored by capital inflows into US financial markets, which contribute to the relative strength of the US dollar. A strong dollar makes imports cheaper for American consumers while reducing the competitiveness of US exports. Over the long run, this dynamic contributed to the shrinking global share of US industrial output and to the loss of manufacturing jobs, as shown below by Figures 3 and 4 respectively.

Figure 3: Share of global manufacturing value added, United States vs China (World Bank, 2025).

Figure 4: Manufacturing employment in the United States (thousands of persons), 1980–2025 (Bureau of Labor Statistics, 2025).

In turn, this has led to a gradual erosion of the US industrial base, including in strategically important sectors such as shipbuilding and defence manufacturing. Therefore, while the international monetary foundations of American hegemony have brought substantial benefits for American consumers, financial markets, and the global projection of US soft power, they have also contributed to weakening some of the productive foundations of American power itself.

The Trump administration appears to have decided for a strategy aimed at bringing industrial output and manufacturing back to the US. Trade deficits, in Trump’s words, represent a “threat to the national security” of the United States, and profoundly harm its economy (EO 14257). The strategy pursued by the Trump administration aims to reduce imports through the introduction of tariffs. At the same time, Trump has repeatedly called on the Federal Reserve to weaken the dollar, a measure that would increase the competitiveness of US exports and stimulate domestic industrial production (Reuters, 2025a).

However, reindustrialising the country may carry deeper consequences for US power projection and the stability of the international system. Reducing the US trade deficit may weaken US dollar centrality in the international economic and financial system, undermining one of the pillars of American power projection. This structural contradiction closely resembles the so-called Triffin dilemma, a concept developed by the economist Robert Triffin in the 1960s. According to the Triffin dilemma, the provision of global liquidity by the issuer of reserve currency requires the continuous supply of reserve assets to the international system, a process typically associated with persistent external imbalances (IMF, 2010).

Trump’s strategy, if thoughtfully and wisely implemented, may result in a stronger US industrial and defence base. However, it appears to run up against the US dollar hegemonic system. In its attempt to reduce US external deficits, the Trump administration risks undermining the centrality of the US dollar in the international system, especially at a time when other countries may begin to question other pillars of dollar dominance, namely the institutional credibility of the United States and its ability to project military power, as evidenced by the difficulties the United States recently encountered in achieving its objectives through the use of force in the Strait of Hormuz (Associated Press, 2026).

4. Strategic Consequences

4.1. Challenges to Dollar Dominance

Trump’s strategy of reducing US external deficits could produce broader systemic consequences for the international economic and financial order. As persistent US external deficits result in a continuous injection of US dollars in the international system, a structural contraction of this supply may reduce the availability of safe dollar assets within the global financial system, potentially encouraging diversification towards alternative monetary and financial arrangements. Although this is a process that had already been underway before Trump’s re-election, his strategy could substantially accelerate it.

In this context, BRICS countries are among the actors seeking to reduce their dependence on the dollar-centred financial system. Brazil, in particular, appears to be pushing for reforms aimed at facilitating international payments in local currencies within the BRICS bloc, thereby reducing dependence on the US dollar and on US-led financial networks (Reuters, 2025b). Along similar lines, China and Russia have promoted the development of alternative cross-border payment infrastructures, notably China’s Cross-Border Interbank Payment System (CIPS) and Russia’s System for Transfer of Financial Messages (SPFS), with the aim of reducing reliance on the Western-dominated SWIFT network (Johnston, 2025, p. 254). Trump, on the other hand, stated that BRICS countries had “no chance” of replacing the US dollar in international trade and threatened to impose tariffs to countries that tried to reduce their reliance on the dollar (Reuters, 2025c). Yet, this position highlights a broader contradiction within his economic strategy, as efforts aimed at reducing external deficits and reindustrialising the American economy may unintentionally weaken some of the structural foundations underpinning the international centrality of the dollar.

However, BRICS countries are not the only actors exploring alternatives to the US dollar. In May 2025, Christine Lagarde, President of the European Central Bank, stated that the euro could potentially emerge as a viable alternative within the international monetary system (Reuters, 2025d). To achieve this objective, she argued that the European Union would first need to undertake significant structural reforms, including deeper financial market integration, common debt issuance, and stronger European defence capabilities (Reuters, 2025d). According to this view, such reforms could enable Europe to provide global investors with a large supply of safe and highly liquid Euro-denominated assets, backed by strong and reliable foundations, while simultaneously benefiting from greater capital inflows and lower borrowing costs (Reuters, 2025d).

4.2. Erosion of US Soft Power and Alliance Cohesion

The international centrality of the US dollar does not solely serve American economic interests. Through the dollar-centred financial system, the United States retains considerable influence over foreign countries’ economic policies and financial conditions. The central role of US financial infrastructures and the dominant position of the dollar in international transactions provide Washington with important geopolitical leverage. For instance, access to dollar funding and to international payment networks can be used by the United States as a tool to exert influence and pressure on foreign governments (Farrell and Newman, 2019). If the strategy pursued by the Trump administration were to result in a weakening of the international role of the dollar, the United States’ soft power and global influence could also gradually erode.

In addition to that, Trump’s strategy and tariff policies are also generating tensions and mistrust among US allied countries and trading partners, while at the same time creating incentives for greater strategic autonomy among them. Reacting to Trump’s 10% global tariffs – together with higher country-specific rates – Australian Prime Minister Anthony Albanese stated that such measures were “not the act of a friend”, while European Commission President Ursula Von der Leyen declared that Europe was prepared to respond with countermeasures if necessary (Reuters, 2025e). Also Canada, one of the United States’ historically closest allies, reacted strongly to the introduction of Trump’s tariffs, criticising the administration’s trade strategy and responding with retaliatory measures on US imports. Japan, in turn, questioned the reliability of its alliance and trade partnership with the US, arguing that tariffs would only contribute to strengthening China’s influence in Southeast Asia (Politico, 2025a).

Finally, the aggressive trade measures adopted by the Trump administration are encouraging US partners, and in particular the European Union, to pursue greater strategic autonomy. In this sense, Europe is seeking to diversify its trade away from the United States by signing new trade agreements with other global actors, such as India and MERCOSUR, and to diversify its energy supplies (Politico, 2025b). In addition, there is renewed momentum in the debate on deepening EU market integration and enhancing defence cooperation, with the aim of reducing internal fragmentation and limiting Washington’s leverage over the continent (CEPR, 2025).

5. Conclusion

The strategy pursued by the Trump administration reflects the perception among large segments of American society that globalisation and trade openness have brought significant damage to US productive and industrial foundations, weakening American power. In this context, tariffs and reindustrialisation policies are presented as necessary instruments to restore domestic industrial capacity, reshore manufacturing jobs, and reduce dependencies from foreign suppliers.

However, the analysis developed in this article suggests that such a strategy may prove difficult to reconcile with the post-Cold War economic and financial order that has sustained American hegemony for decades. US trade deficits should not be seen solely as the result of domestic commercial and industrial policy failures, but rather as a structural feature of an international monetary system centred on the global role of the US dollar and the continuous provision of dollar liquidity to the world economy. Reducing these imbalances may therefore produce significant transformations within the international system and potentially weaken some of the foundations of US global influence.

At the same time, Trump’s policies have generated tensions with allies and trading partners, while also encouraging efforts aimed at reducing dependence on the United States. BRICS countries appear increasingly determined to promote alternative and more autonomous international payment systems, while the European Union is reconsidering its reliance on the United States in areas such as trade and defence. These dynamics could contribute to a further erosion of the international role of the US dollar and, more broadly, of American geopolitical leverage worldwide.

Ultimately, the Trump administration appears to be confronting a broader strategic dilemma: how to restore the productive foundations of American power without simultaneously undermining the international pillars that have long sustained US global hegemony.

References

Associated Press (2026) Trump, Iran pressure campaign and Strait of Hormuz tensions, AP News. Available at: https://apnews.com/article/trump-iran-pressure-campaign-strait-hormuz-de-8166b4d513523ee8b73ff058210dc581.

BEA (2025) International Trade in Goods and Services. U.S. Bureau of Economic Analysis. Available at: https://www.bea.gov/data/intl-trade-investment/international-trade-goods-and-services.

CEPR (2025) Strategic autonomy for Europe requires economic growth. VoxEU Column, 4 September 2025. Available at: https://cepr.org/voxeu/columns/strategic-autonomy-europe-requires-economic-growth#:~:text=This%20column%2C%20taken%20from%20a%20CE.

CSIS (2025) China Dominates the Shipbuilding Industry. Center for Strategic and International Studies. Available at: https://www.csis.org/analysis/china-dominates-shipbuilding-industry?utm_source.

Eichengreen, B. (2011) Exorbitant privilege: The rise and fall of the dollar and the future of the international monetary system. Oxford: Oxford University Press.

European Central Bank (ECB) (2023) Globalisation, inflation and the euro area economy. Economic Bulletin, Focus (Box/ECB Focus Article). Available at: https://www.ecb.europa.eu/press/economic-bulletin/focus/2023/html/ecb.ebbox202301_02~8d6f1214ae.en.html?utm_sour.

Farrell, H. and Newman, A. L. (2019) ‘Weaponized interdependence: how global economic networks shape state coercion’, International Security, 44(1), pp. 42–79. Available at: https://direct.mit.edu/isec/article/44/1/42/12237/Weaponized-Interdependence-How-Global-Economic.

Federal Reserve Board (2022) International spillovers of tighter monetary policy. FEDS Notes, 22 December. Available at: https://www.federalreserve.gov/econres/notes/feds-notes/international-spillovers-of-tighter-monetary-policy-20221222.html.

FRED (2025a) Federal Debt Held by the Public as Percent of Gross Domestic Product (FYGFGDQ188S). Federal Reserve Bank of St. Louis. Available at: https://fred.stlouisfed.org/series/FYGFGDQ188S.

FRED (2025b) 10-Year Treasury Constant Maturity Rate (DGS10). Federal Reserve Bank of St. Louis. Available at: https://fred.stlouisfed.org/series/DGS10.

FRED (2025c) U.S. Dollars to Euro Spot Exchange Rate (DEXUSEU). Board of Governors of the Federal Reserve System (US), H.10 Foreign Exchange Rates. Federal Reserve Bank of St. Louis. Available at: https://fred.stlouisfed.org/series/DEXUSEU.

FRED (2025d) U.S. Dollars to U.K. Pound Sterling Spot Exchange Rate (DEXUSUK). Board of Governors of the Federal Reserve System (US), H.10 Foreign Exchange Rates. Federal Reserve Bank of St. Louis. Available at: https://fred.stlouisfed.org/series/DEXUSUK.

International Monetary Fund (2010) Reserve Accumulation and International Monetary Stability. Washington, DC: International Monetary Fund.

International Monetary Fund (IMF) (2025) Currency Composition of Official Foreign Exchange Reserves (COFER). Available at: https://data.imf.org/en/Datasets/COFER.

Johnston, L.A. (2025) The BRICS, the dollar and SWIFT: A review of evolving interests and monetary reform momentum. Available at: https://www.tandfonline.com/doi/full/10.1080/10220461.2025.2523509.

Krugman, P.R., Obstfeld, M. and Melitz, M.J. (2018) International Economics: Theory and Policy. 11th edn. Boston: Pearson.

Meyermans, E. (2014) The ‘exorbitant privilege’ of an international-currency status: theory and evidence, in European Commission, DG ECFIN, Quarterly Report on the Euro Area, Chapter IV.

Obstfeld, M. and Rogoff, K.S. (2005) ‘Global current account imbalances and exchange rate adjustments’. Brookings Papers on Economic Activity, 2005(1), pp. 67–146.

Obstfeld, Maurice (2015). Trilemmas and Trade-offs: Living with Financial Globalisation. BIS Working Papers No. 480, Bank for International Settlements.

Politico (2025a) Trump’s tariff letters roil Asian allies. 8 July. Available at: https://www.politico.com/news/2025/07/08/trumps-tariff-letters-roil-asian-allies-00443008?utm_source.

Politico (2025b) Europe begins retreat from US dependence as Trump rocks transatlantic relationship. Politico.eu. Available at: https://www.politico.eu/article/europe-begins-retreat-united-states-dependence-donald-trump-rocks-transatlantic-relationship/.

Reuters (2025a) Fed should cut interest rate by a full point, Trump says. 6 June 2025. Available at: https://www.reuters.com/world/us/fed-should-cut-interest-rate-by-full-point-trump-says-2025-06-06/?utm_source.

Reuters (2025b) Brazil nixes BRICS currency, eyes less reliance on ‘mighty’ dollar. 13 February. Available at: https://www.reuters.com/markets/currencies/brazil-nixes-brics-currency-eyes-less-reliance-mighty-dollar-2025-02-13/.

Reuters (2025c) Trump repeats tariffs threat to dissuade BRICS nations from replacing US dollar. 31 January. Available at: https://www.reuters.com/markets/currencies/trump-repeats-tariffs-threat-dissuade-brics-nations-replacing-us-dollar-2025-01-31/?utm_source.

Reuters (2025d) Euro could become the dollar’s alternative, Lagarde says. 26 May. Available at: https://www.reuters.com/world/europe/euro-could-become-dollars-alternative-lagarde-says-2025-05-26/?utm_source.

Reuters (2025e) World leaders condemn Trump’s tariffs, some pledge retaliation. 3 April. Available at: https://www.reuters.com/world/world-leaders-condemn-trumps-tariffs-some-pledge-retaliation-2025-04-03/.

Rogoff, K.S. and Tashiro, T. (2015) Japan’s Exorbitant Privilege. Journal of the Japanese and International Economies, 35, pp. 43–61. Available at: https://www.sciencedirect.com/science/article/pii/S0889158314000641?via%3Dihub.

U.S. Bureau of Labor Statistics (n.d.) All Employees, Manufacturing (MANEMP). Federal Reserve Economic Data (FRED), Federal Reserve Bank of St. Louis. Available at: https://fred.stlouisfed.org/series/MANEMP?utm_source.

U.S. Federal Register (2025) Executive Order 14257 of April 2, 2025: Regulating Imports With a Reciprocal Tariff to Rectify Trade Practices That Contribute to Large and Persistent Annual United States Goods Trade Deficits. Available at: https://www.federalregister.gov/documents/2025/04/07/2025-06063/regulating-imports-with-a-reciprocal-tariff-to-rectify-trade-practices-that-contribute-to-large-and.

U.S. Federal Register (2025) Proclamation 10947 of June 3, 2025: Adjusting Imports of Aluminum and Steel into the United States. Vol. 90, No. 109. Available at: https://www.federalregister.gov/documents/2025/06/09/2025-10524/adjusting-imports-of-aluminum-and-steel-into-the-united-states.

World Bank (n.d.) Manufacturing, value added (current US$) – NV.IND.MANF.CD. World Development Indicators. Available at: https://data.worldbank.org/indicator/NV.IND.MANF.CD.

World Bank (2025) PPP conversion factor, GDP (LCU per international $) (PA.NUS.PPP). International Comparison Program. Available at: https://data.worldbank.org/indicator/PA.NUS.PPP?utm_source.

Zoffer, J.P. (2019) The Dollar and the United States’ Exorbitant Power to Sanction. AJIL Unbound, Cambridge University Press.